Underhyping Snapchat

The media, analyst and investor communities clearly have a love-hate relationship with Snapchat. In the run-up to its IPO, it was hailed as the next great technology company (in part due to Snap's own communication efforts). And now that its S-1 is out, the commentary has turned quite negative. As always, the truth is somewhere in the middle and public filings paint a very clear picture of why that is.

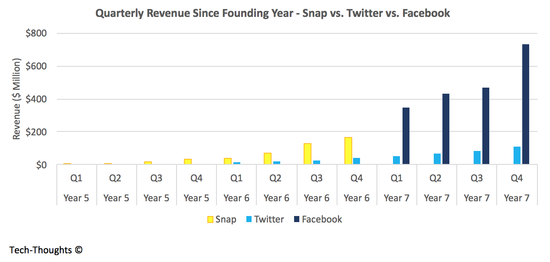

The chart at the top of this post shows quarterly revenue for Snap compared with that of Twitter and Facebook, aligned by founding year (sourced from their respective IPO prospectuses). The first observation is that Snap is going public earlier in its lifecycle than both Facebook and Twitter. Of course, this is partially offset by the fact that Snap was conceived during the "post-PC" smartphone revolution, which accelerated consumer adoption cycles, especially for social media. That said, Snap's advertiser adoption seems to be growing at roughly as the same pace as its predecessors (at the same point in their respective lifecycles), which is more relevant for a revenue comparison. Taking these factors and the chart into account, it looks like Snap's revenue growth is slightly behind Facebook's pace and well ahead of Twitter's.

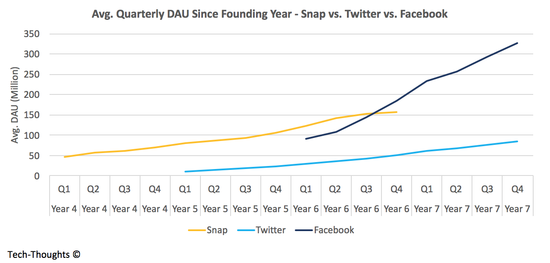

Now, what's driving this revenue growth? User growth and ad engagement. The chart below shows average daily active users for each of the three companies, aligned by founding year (Twitter only reported DAU for one period in its IPO prospectus, so I had to use a few assumptions built on top of Facebook's historical DAU/MAU ratio at the same point in its lifecycle to estimate these).

Clearly, user growth is the metric that has scared tech and investor communities alike. Despite all the advantages the smartphone revolution presented, Snap's user trajectory looks meaningfully flatter than Facebook's. While Snap's DAU figures are certainly higher that Twitter's were at the same point, its growth trajectory is only slightly better. Also, Snap's user growth slowed even further after Q3 when Instagram added the "Stories" feature than Snapchat had pioneered. The competitive dynamic with Instagram is certainly concerning when it comes to user growth, but there is little evidence to suggest an impact on aggregate engagement from Snapchat's existing users. Instagram already owns a vast international userbase and the presence of Instagram stories obviates the need to experiment with Snapchat (especially with Snapchat's daunting UI compared to Instagram's easy onboarding experience).

So based on existing evidence, it would be safe to assume that Snapchat's steady state user base is not likely to challenge Facebook or Instagram, even if it is somewhat larger than Twitter. This isn't necessarily bad simply because of the kind of users Snapchat tends to attract. We have heard enough about Snapchat's hold on teens in the US, but Snapchat's aforementioned daunting UI is even more important. The first screen presented to users when they open Snapchat is a camera screen (as compared to a "feed" or option to follow friends). This is a deliberate decision to ensure that a significant portion of their user base not only consumes content, but creates it. This is antithetical to the engagement patterns on most social networks, including Facebook and Twitter, where content creators tend to be a very small portion of the user base. By extension, the average Snapchat user should be more engaged and, therefore, more valuable over time than the average Facebook or Instagram user.

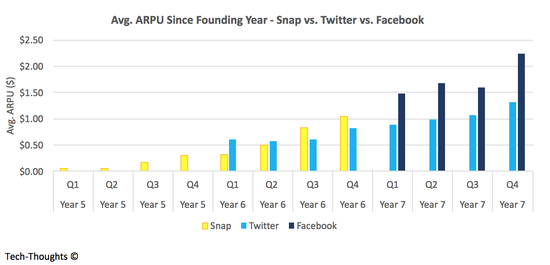

While we don't have public user engagement or ad engagement data to confirm this hypothesis, we do have something to benchmark this against. The chart below shows average revenue per user for the three companies (using quarterly revenue and average daily active users during the quarter).

Snap's ARPU trajectory looks quite healthy and roughly on pace with where Facebook would have been. It is complicated to draw a direct relationship between ARPU and ad engagement since we still don't have specific figures on ad load, i.e. the number of ads each user is exposed to. At the very least, it does show healthy growth in the company's advertising business. Over the next few years, video will likely morph into Snap's key advantages over rival networks. While Facebook, Twitter and Instagram have been attempting to move into video and video advertising, the nature of engagement with the "feed" is "scroll"-centric. Users are more likely to quickly see snippets of content and scroll past, rather than engage with discrete bits of content for a length of time. This is a poor fit with video consumption habits and TV advertising (where a majority of ad dollars are still allocated). However, Snapchat's full screen video and lenses lead to deeper engagement, which is a better fit for TV advertisers. Of course, YouTube and, to some extent, Instagram (via Stories) will receive significant portions of the current TV ad budget over time. But Snapchat's hold on US teens will guarantee that it gets a fair share.

On the whole, we can clearly see that Snap still has significant room for revenue growth even if its user growth remains muted. While this may not be quite the outcome some expected, it is still a good enough story for a successful IPO.

This story was reposted with permission from tech-thoughts

Sameer Singh is an M&A professional and business strategy consultant focusing on the mobile technology sector. He is founder and editor of tech-thoughts.net.

Sameer Singh is an M&A professional and business strategy consultant focusing on the mobile technology sector. He is founder and editor of tech-thoughts.net.